Roofing

How to Get Your Insurance to Pay for a Roof Replacement: 8 Simple Steps

How to Get Your Insurance to Pay for a New Roof: 8 Simple Steps

If your roof has suffered damage, it’s crucial to replace it quickly. Wondering how to get your insurance company to cover the cost of a new roof? Follow these eight easy steps to navigate the process and increase your chances of approval.

Whether your roof was damaged by a storm or is simply in need of repair, the cost can be overwhelming. However, your insurance company might be able to help. Although working with your insurer can seem daunting, we’ve simplified the process for you.

In this guide, we’ll walk you through five straightforward steps to file a claim, provide helpful tips from insurance experts, and share advice on how to prevent roof damage in the future.

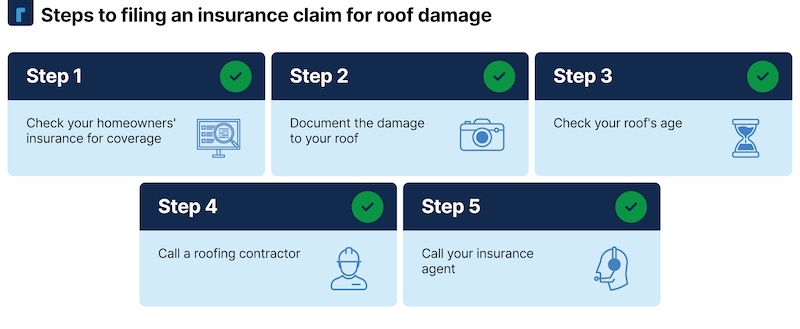

Step 1: Review Your Homeowners’ Insurance for Coverage

Before anything else, take a close look at your homeowners’ insurance policy. Not all roof damages are covered, so it’s essential to understand what is and isn’t included. For example, basic homeowners’ policies in Florida may not cover wind damage, and wildfires aren’t typically covered in California, as noted by Colleen Parsons, client advisor at World Insurance Associates. These types of coverage usually require additional policies and come with a higher cost.

If your policy explicitly excludes roof repairs, you may not be able to make a claim. However, if there’s ambiguity in the coverage, you might still be able to get partial compensation for the damage. Be sure to fully understand your coverage and your deductible before filing a claim.

Commonly Covered Damages:

- Damage from severe weather

- Fire damage

- Hail damage

What’s Not Covered:

- Neglect or lack of proper maintenance

- Normal wear and tear

- Improper installation

- Mold, mildew, or moss growth

Step 2: Document the Damage

Take photos of the damage as soon as possible, ensuring you stay safe while doing so. Capture any visible damage, such as scattered shingles or tree branches on the roof. The more photos you have, the stronger your claim will be. Timestamped photos along with a weather report can also provide evidence that the damage occurred during a significant weather event.

Step 3: Check the Age of Your Roof

The age of your roof plays a significant role in your claim. Roofs less than ten years old are often fully covered under warranty, but older roofs may only receive a depreciated value for repairs or replacements. This means your insurance payout could be less than what you expect.

Step 4: Contact a Roofing Contractor

If the damage requires immediate attention, such as leaks during a storm, reach out to a roofing contractor first. It’s best to call a roofer early, especially if a storm has caused widespread damage and local companies are in high demand. The roofer will assess the damage, provide documentation, and give you an estimate to present to the insurance adjuster.

Even if there’s no emergency, a roofing contractor can still help you by giving an accurate assessment of the damage and potential repair costs.

Remember to get multiple quotes, especially if you’re unfamiliar with roofing contractors. This ensures you get the best possible price and avoid potential scams. Be wary of offers that seem too good to be true, like waived deductibles or promises of a “free roof,” as these may be scams. It’s also illegal for a roofer to waive your deductible.

Step 5: Contact Your Insurance Agent

Courtesy of Fixr

Before you call the insurance company’s claims department, have a discussion with your insurance agent. Consider the age of your roof, the severity of the damage, your deductible, and how filing a claim might impact your future premiums. This conversation will help you decide whether filing a claim is worth it or if paying out of pocket might be a better option.

If you decide to move forward with a claim, your agent will assist you in filing it. If you need to make an emergency claim outside of business hours, call the company’s claims number immediately. Be sure to file your claim within 30 days to avoid having it denied due to delays.

Step 6: Protect Your Roof Moving Forward

After replacing your roof, it’s essential to take steps to prevent future damage. Regular roof maintenance, such as cleaning debris and ensuring proper water drainage, can help extend the life of your roof. Routine inspections will also allow you to address issues before they become costly problems.

Step 7: Understand Insurance Complaints and Concerns

While dealing with insurance companies, you may hear complaints from others, like how an insurer dropped their policy or raised their rates after a claim. Keep in mind that, in some cases, an insurer may drop coverage if your roof is old or severely damaged, as they may view it as a risk. As Parsons explains, insurers want to ensure you maintain your home properly, as they’re not a maintenance service.

Additionally, while homeowners insurance doesn’t typically surcharge for claims like auto insurance, rates can still rise due to increasing costs or the potential for future claims, as noted by Guttman.

Step 8: Beware of Storm Chasers

“Storm chasers” are a real concern, especially after major weather events. These companies may appear offering low rates or enticing deals but are often unreliable or outright dishonest. Always choose a local, trusted roofing contractor recommended by someone you know.

Conclusion: Getting Your Roof Back in Shape

If a storm has damaged your roof, following these steps will help you navigate the claims process and get your roof repaired quickly. Whether it’s dealing with your insurance company, contacting the right contractor, or taking measures to protect your roof in the future, this guide provides the tools you need to get your home back to normal.

Need help finding a local roofer to assess your roof damage? Let us assist you in locating a reputable contractor in your area.